West Africa dominates the agri-tech startup space – home to two of the three largest startup ecosystems active in this sector, a new report has stated.

According to the ‘Agrinnovating for Africa: Exploring the African Agri-Tech Startup Ecosystem Report 2018’, the region accounts for 44 per cent of Africa’s agri-tech startups, spread across six countries.

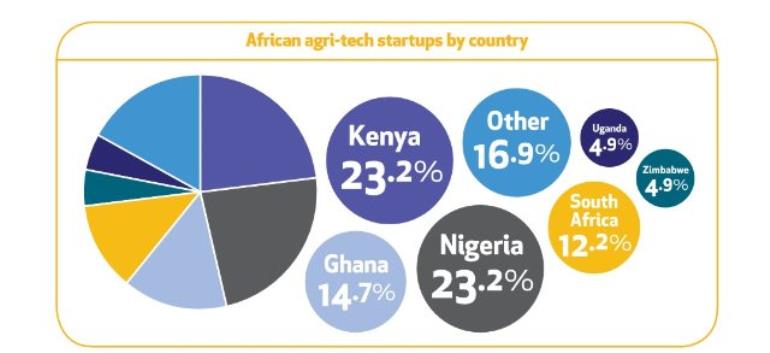

Unsurprisingly, Nigeria is the key contender in the West African region and is tied-first place across the whole African continent (with Kenya).

It houses 19 agri-tech startups – 23.2 per cent of the continent’s total number of ventures active in this space.

Ghana ranks as the second biggest agri-tech ecosystem in the region, and third place in Africa. It has 12 agri-tech ventures, making up 14.7 per cent of the continent’s total.

Active startups were also recorded in The Gambia, which is beginning to emerge as a solid agri-tech market in the region; ahead of the surprisingly limited agri-tech startup activity traced in the Ivory Coast, Senegal, and Cameroon.

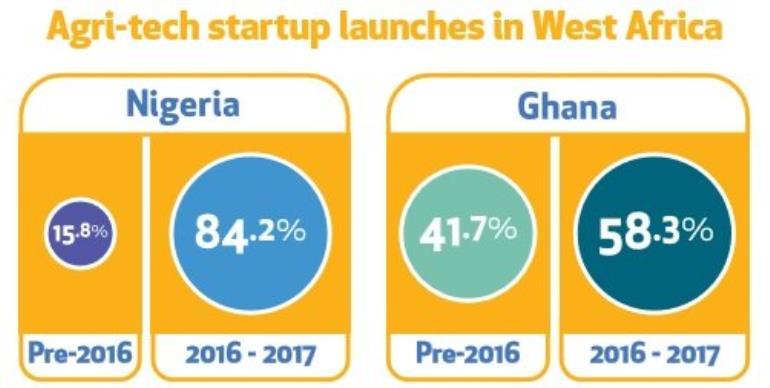

However, this strong West African presence in the agri-tech space is a rather new phenomenon. Only three of Nigeria’s 19 startups were founded pre-2016, evidencing a sudden boom in interest in the agritech space.

In a similar pattern, seven of Ghana’s 12 startups were launched in 2016 and 2017. However, unlike Nigeria, Ghana is also home to a couple of older startups which formed as far back as 2012.

Interestingly, the most popular sub-categories of the agri-tech space differ considerably between Nigeria and Ghana – a prime example of the substantial market variations at play in Africa, even within regional neighbours.

In Nigeria, the e-commerce sector is by far the most active area for agri-tech ventures, accounting for 47.4 per cent of the country’s total agri-tech startups. The Nigerian startups in this space vary from online stores for farmers to purchase inputs and equipment; to peer-to-peer marketplaces for smallholders to sell produce.

Fintech for farmers is also popular in Nigeria, with 26.3 per cent of startups working in this space; as is the information and knowledge sharing sub-sector with 21 per cent of startups. The remaining startups are spread across farm and supply chain management, IoT / AI for farmers, and “other”.

Contrast this to Ghana, where an equal number (two) of startups operate across six sub-sectors: fintech for farmers; land ownership; e-commerce; information and knowledge sharing; farm and supply chain management; and IoT / AI for farmers.

It is notable, that Ghana leads the way on the continent with land ownership startups, home to two of the three companies on the continent pioneering innovation in this area.

As looked at in further detail in the “Funding” section of this report, Nigerian and Ghanaian agri-tech startups attract a sizeable amount of investor backing – an understandable fact given the established nature of their ecosystems, and the correlated increasing investor familiarity with these markets.

With a population in excess of 186 million and agriculture the primary economic activity for the majority of the country, the business case for agri-tech in Nigeria makes itself. Add in the country’s techpreneurship prowess, and the scene is set for success. As such it is no wonder that entrepreneurs and investors alike are turning their attention to the agri-tech space.

While access to markets is undeniably a big challenge for farmers across Africa, Nigeria’s mass preference for launching agri-focused e-commerce platforms is perhaps slightly misguided. The obstacles hindering the prosperity of smallholder farmers across Nigeria and the continent are sizeable and very numerous – as such local entrepreneurs would do well to spread their focus to other, equally pressing, areas.

Ghana was an early entrant to the agri-tech scene, however, this has not really translated into any first-mover advantage – other than to establish it as a well-respected player capable of holding its own alongside its far, far bigger neighbour.

To the credit of Ghana’s entrepreneurs, the agri-tech startups coming out of the country seem to have a heightened awareness of the breadth of challenges smallholder farmers face; and between them, these startups are putting up a strong attempt at providing viable solutions to most of these stumbling blocks.

The country does have a solid crop of good companies, and investors are increasingly willing to put money into Ghanaian ventures – as such the country is well-placed to build up a thriving, profitable startup-led agri-tech sector.

As for the rest of West Africa, it is only a matter of time. The initial interest in agri-tech of entrepreneurs in rapidly emerging markets such as Ivory Coast, Senegal and Cameroon are a little disappointing, given the relevance and the potential impact it has their respective countries.

However, with most West African governments putting in place initiatives to promote the agricultural industry, and as local entrepreneurship ecosystems develop, the agri-tech space will undoubtedly grow around the region.

- NOSIBLE Raises $1m Pre-Seed Investment - 03/28/2025

- Equator Secures $55M to Boost Climate Tech Startups in Africa - 03/11/2025

- How to Start a Successful T-Shirt Printing Business? - 03/08/2025